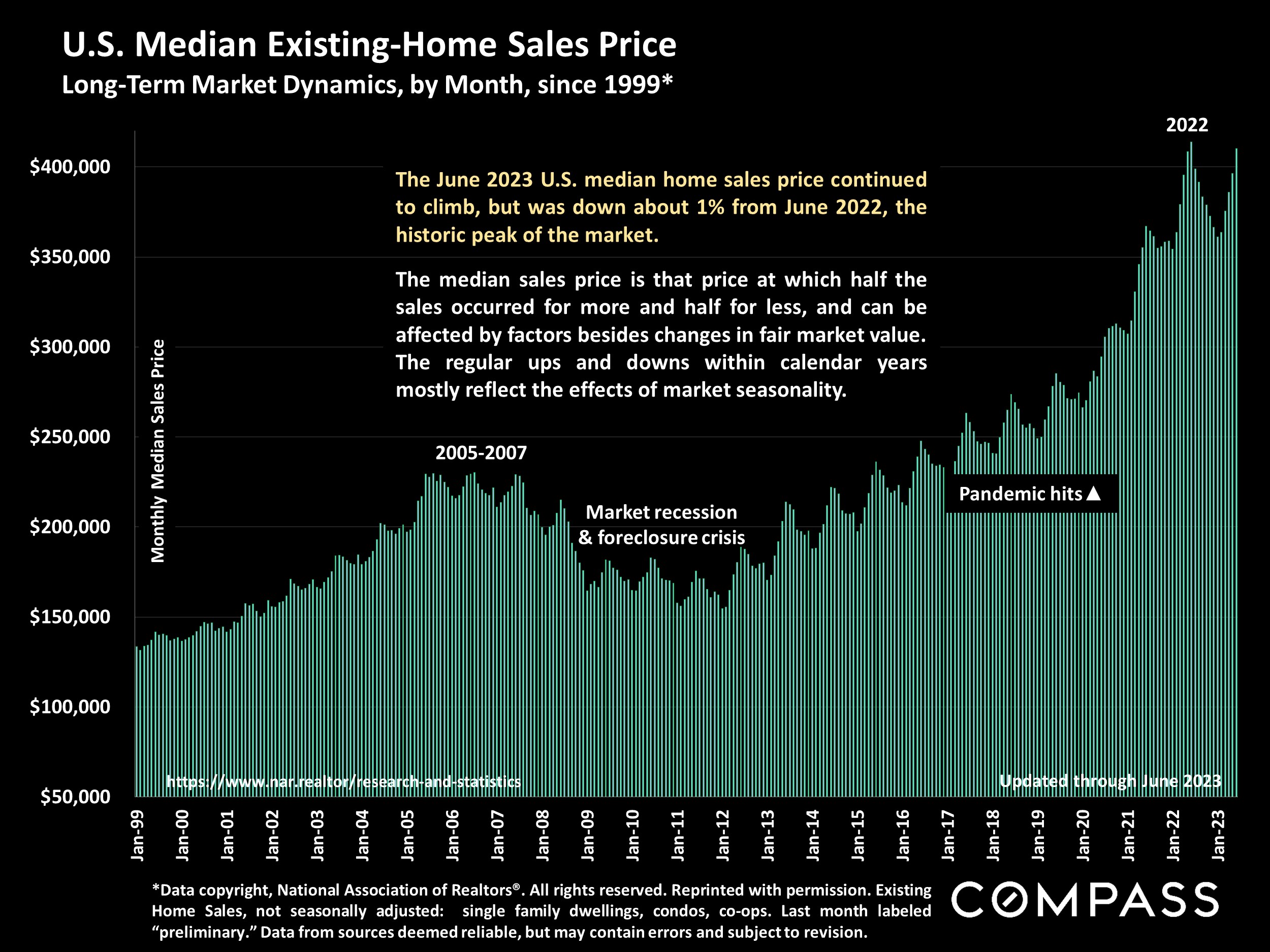

An illustration of long-term, national median home sales prices: The June 2023 price was just 1% lower than in June 2022, the historic peak of the market.

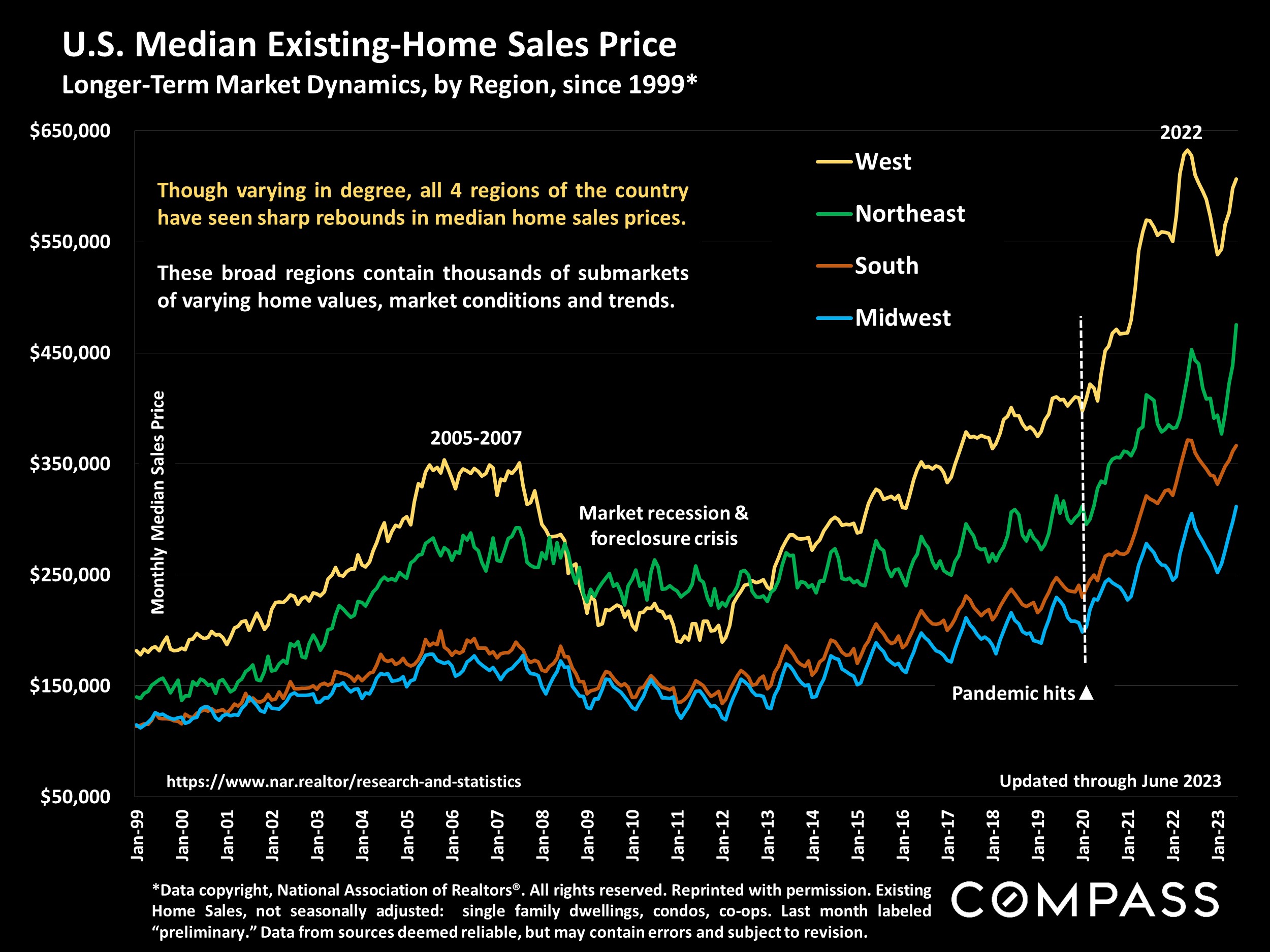

Regional home-price trends generally run roughly parallel over the longer-term, though varying in degree of change within periods due to local conditions.

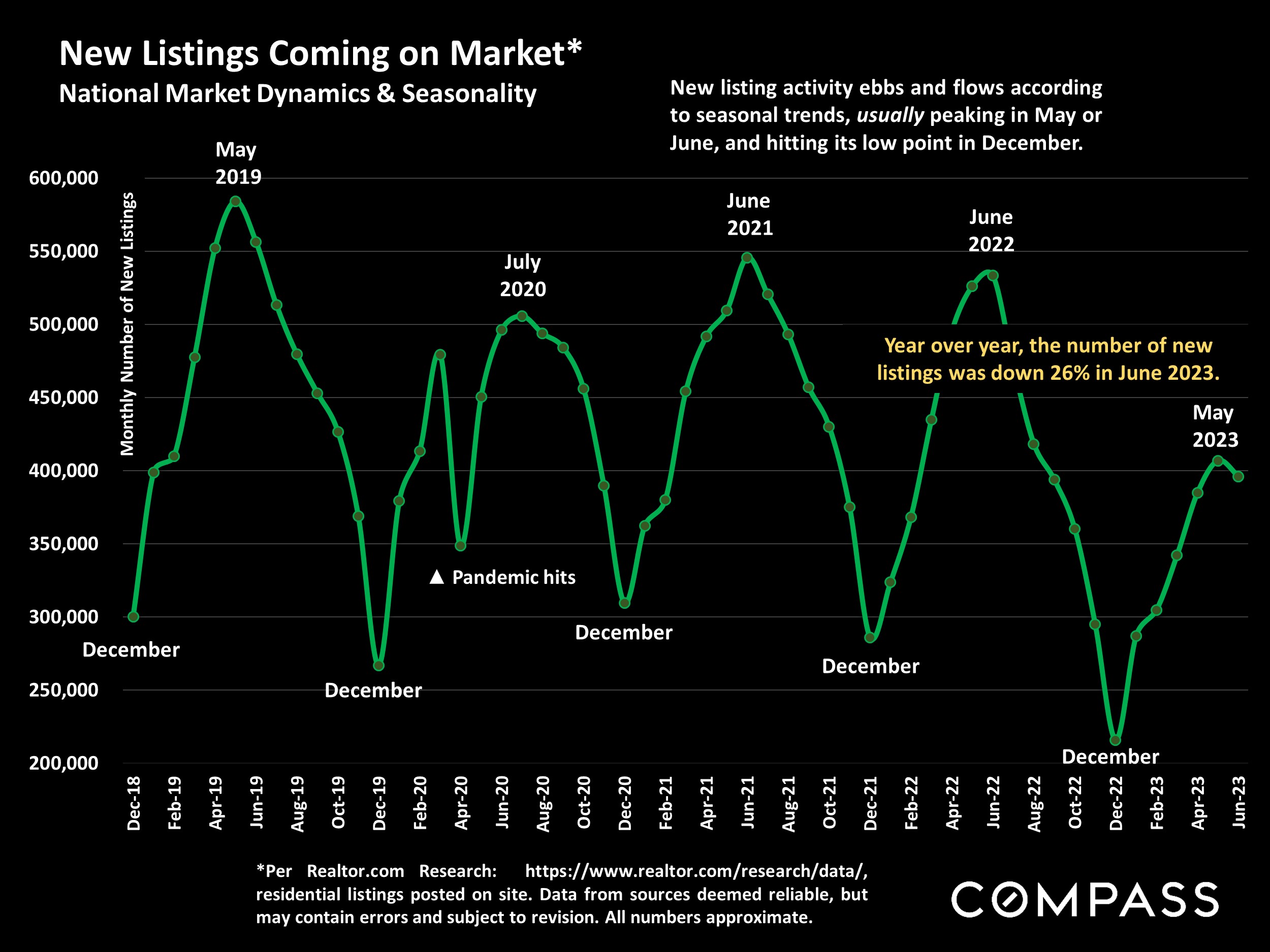

Over the past year, the severe, cumulative decline in the number of new listings has had major ramifications for market dynamics, and, in 2023, contributed to upward pressure on home prices.

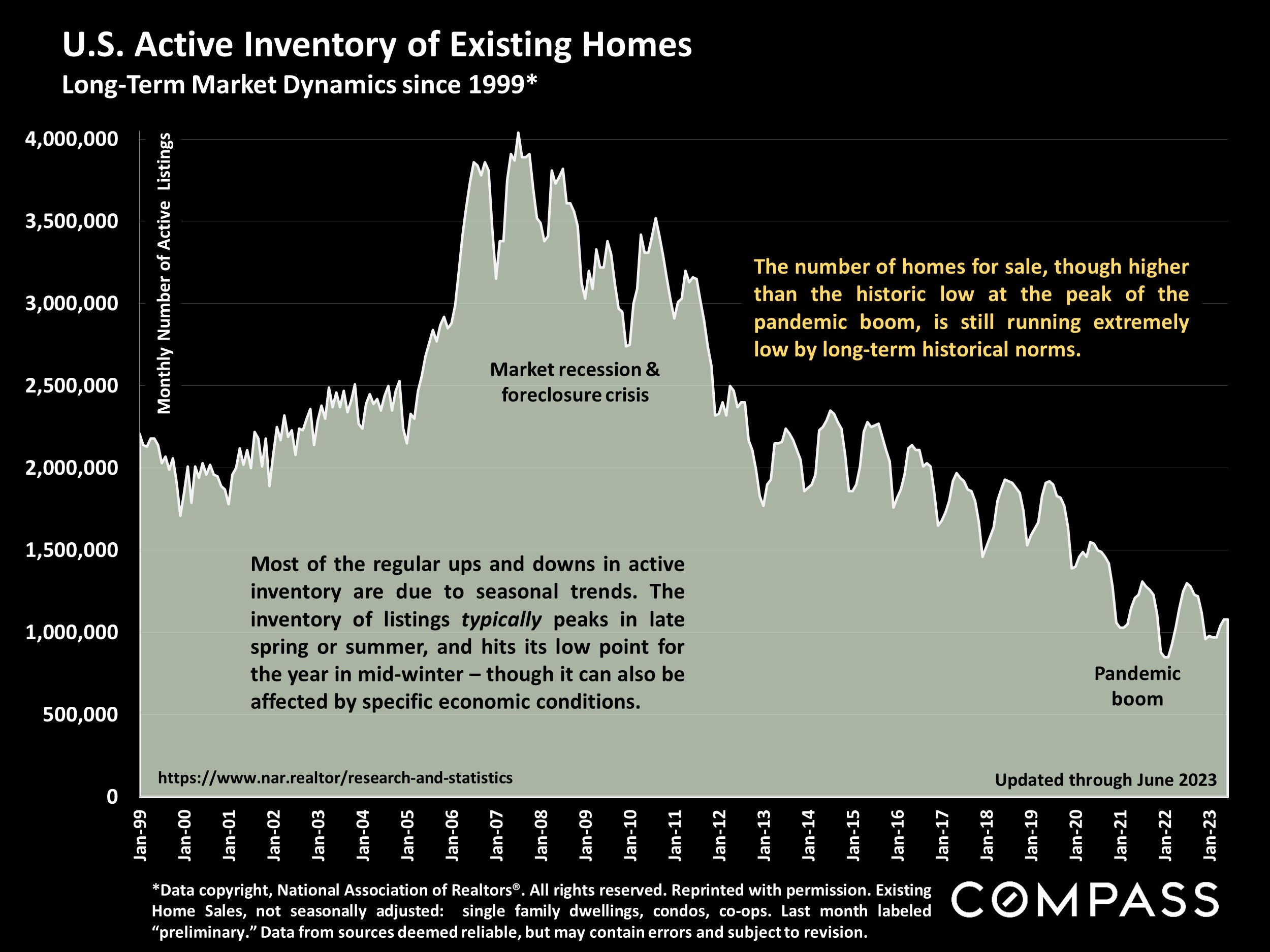

The number of homes for sale remains very low, clearly inadequate to demand. Besides general economic factors, it ebbs and flows according to seasonal trends.

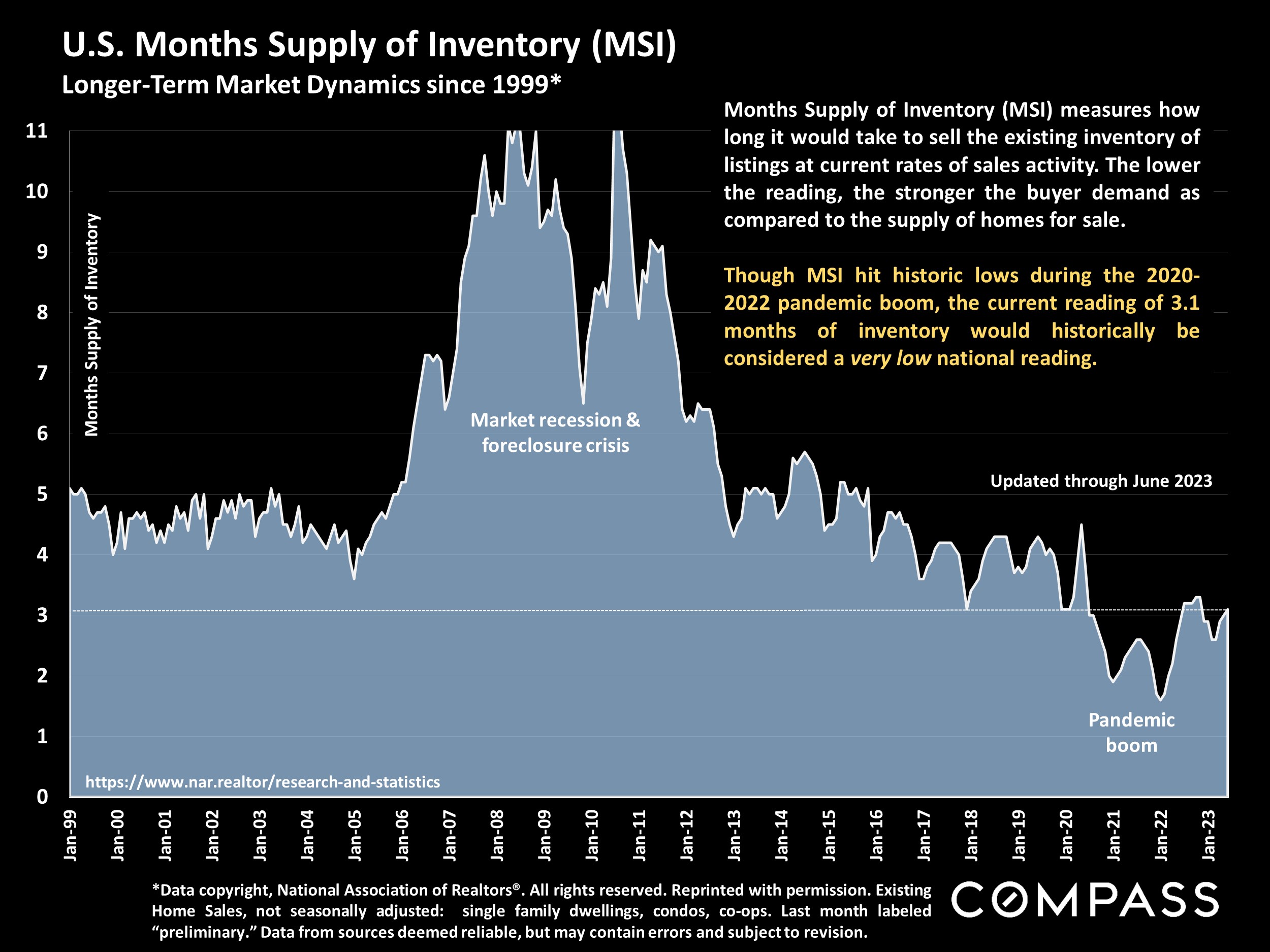

Months-supply-of-inventory compares the supply of listings to buyer demand: Lower readings commonly signify more competitive, more heated markets.

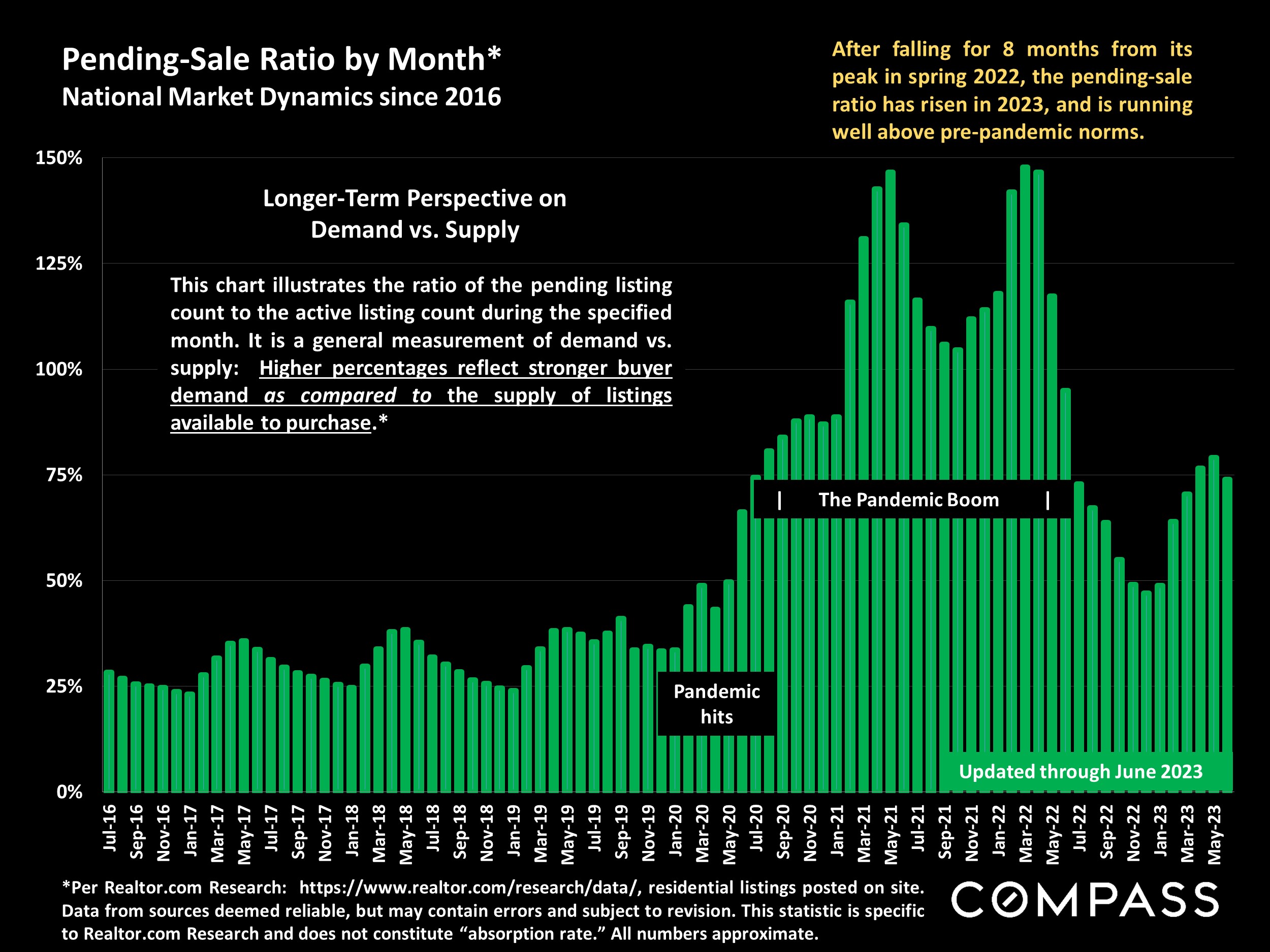

The ratio of pending listings (in contract) to active listings is another angle on supply and demand: Higher readings signify more competitive market conditions.

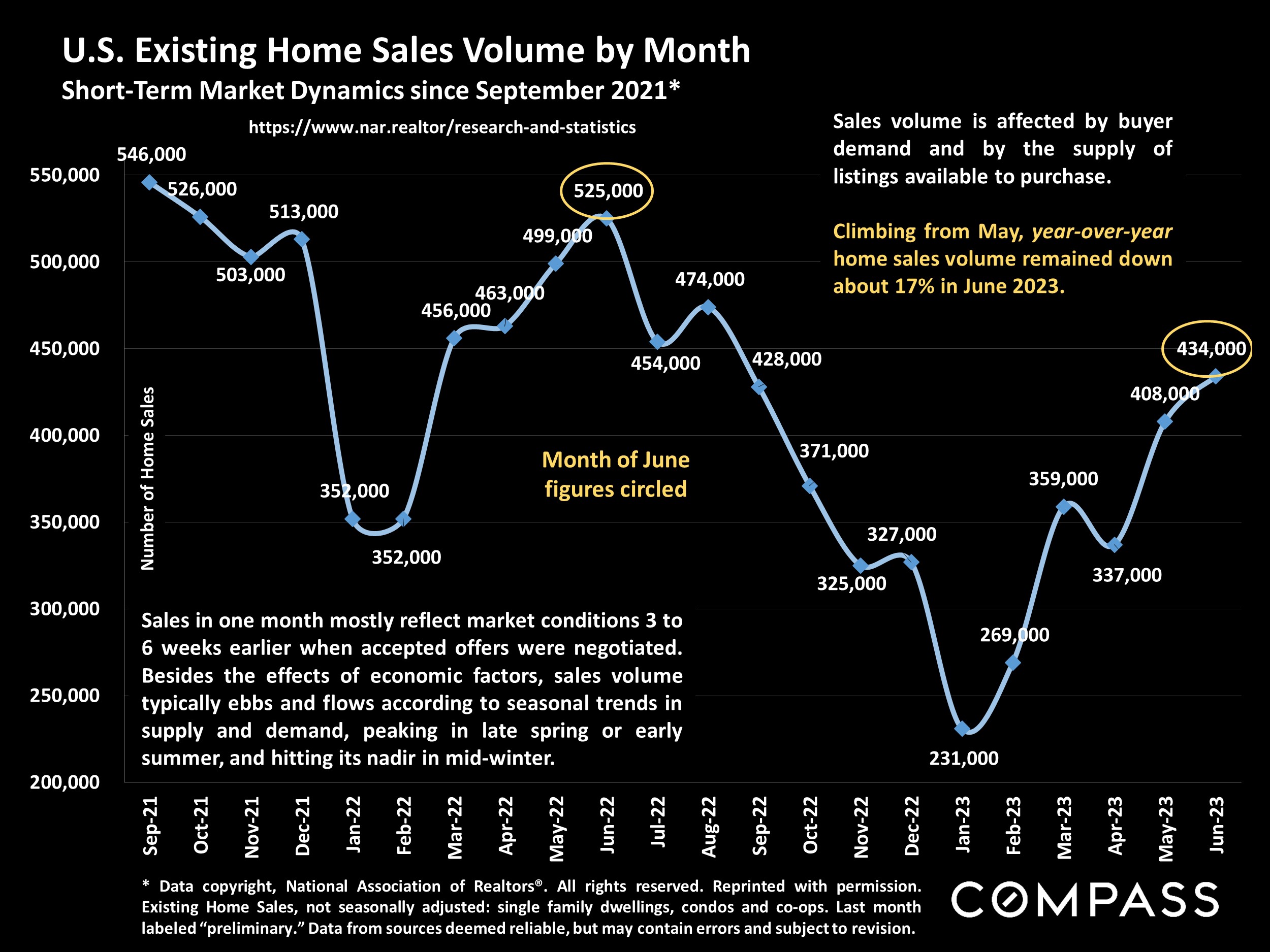

The number of home sales has rebounded from the nadir of late 2022, but remains depressed, lower than historical norms, largely due to the decline in new listings.

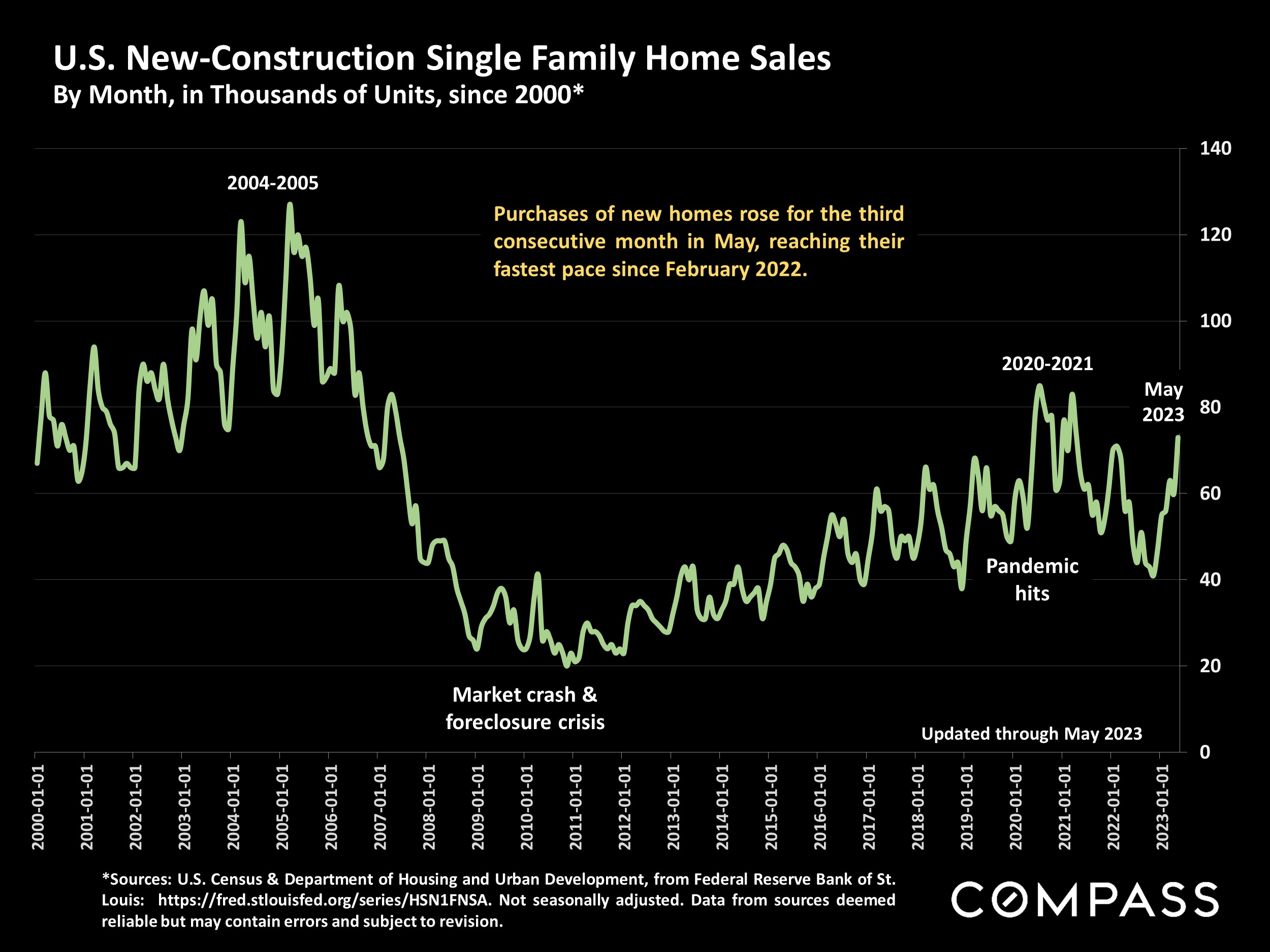

While many homeowners have held back from listing their homes in the past year, developers are quickly increasing the construction of new homes - and sales.

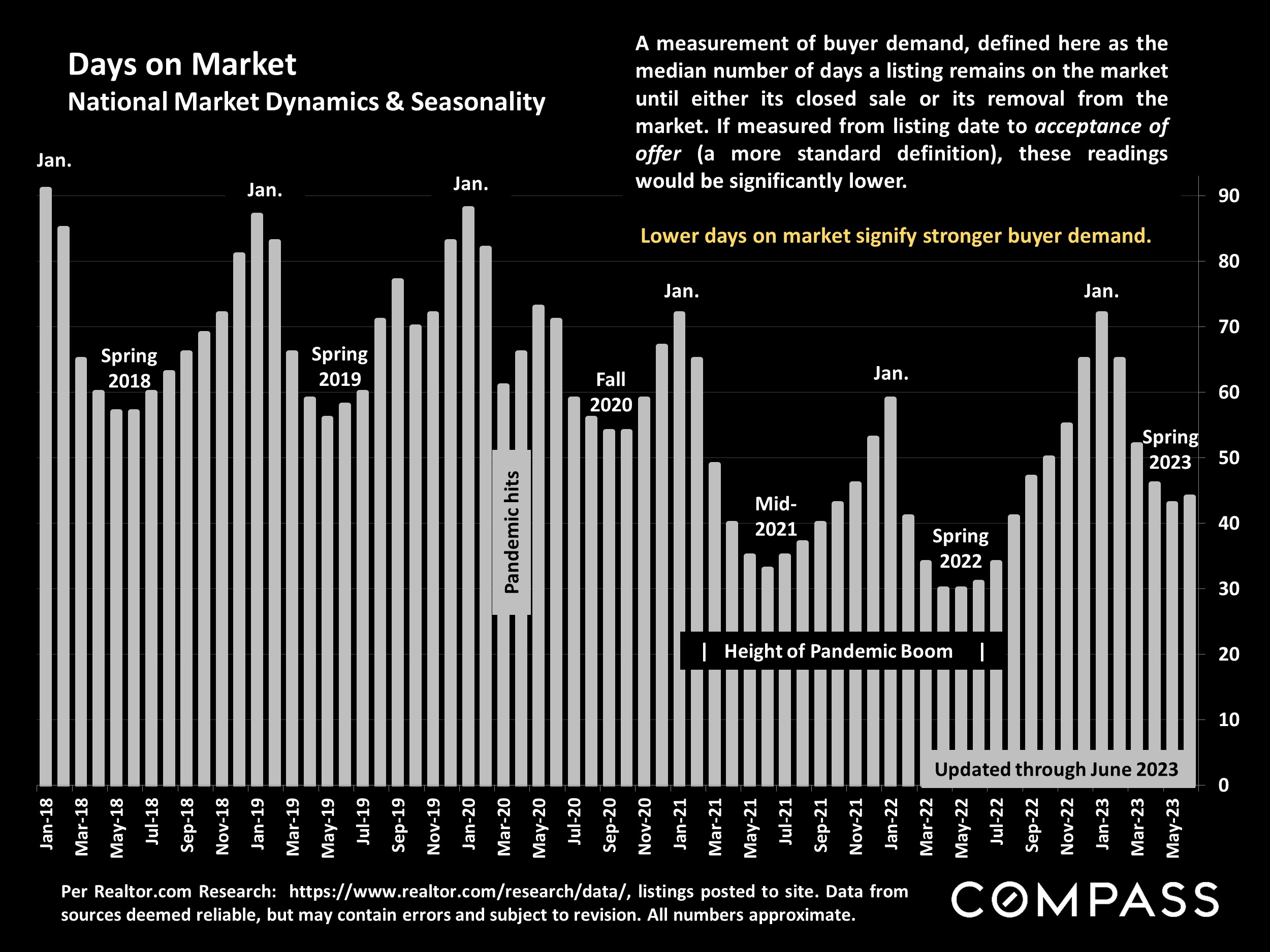

Days on market are currently higher than during the pandemic boom, but lower than historical norms. As with most indicators, they fluctuate by season.

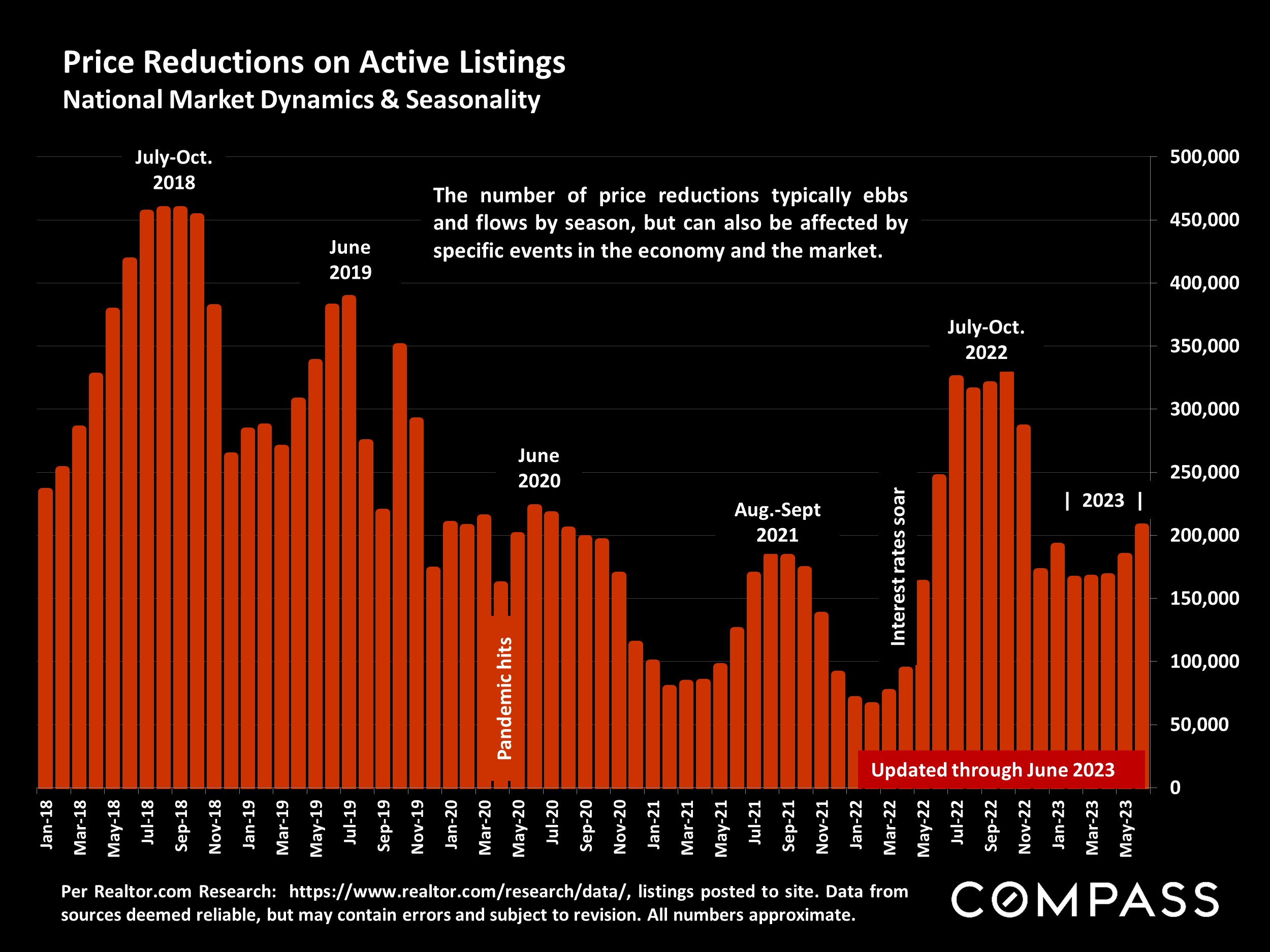

Price reductions rise and fall per sudden changes in economic conditions, and, more regularly, per seasonal trends in supply and demand.

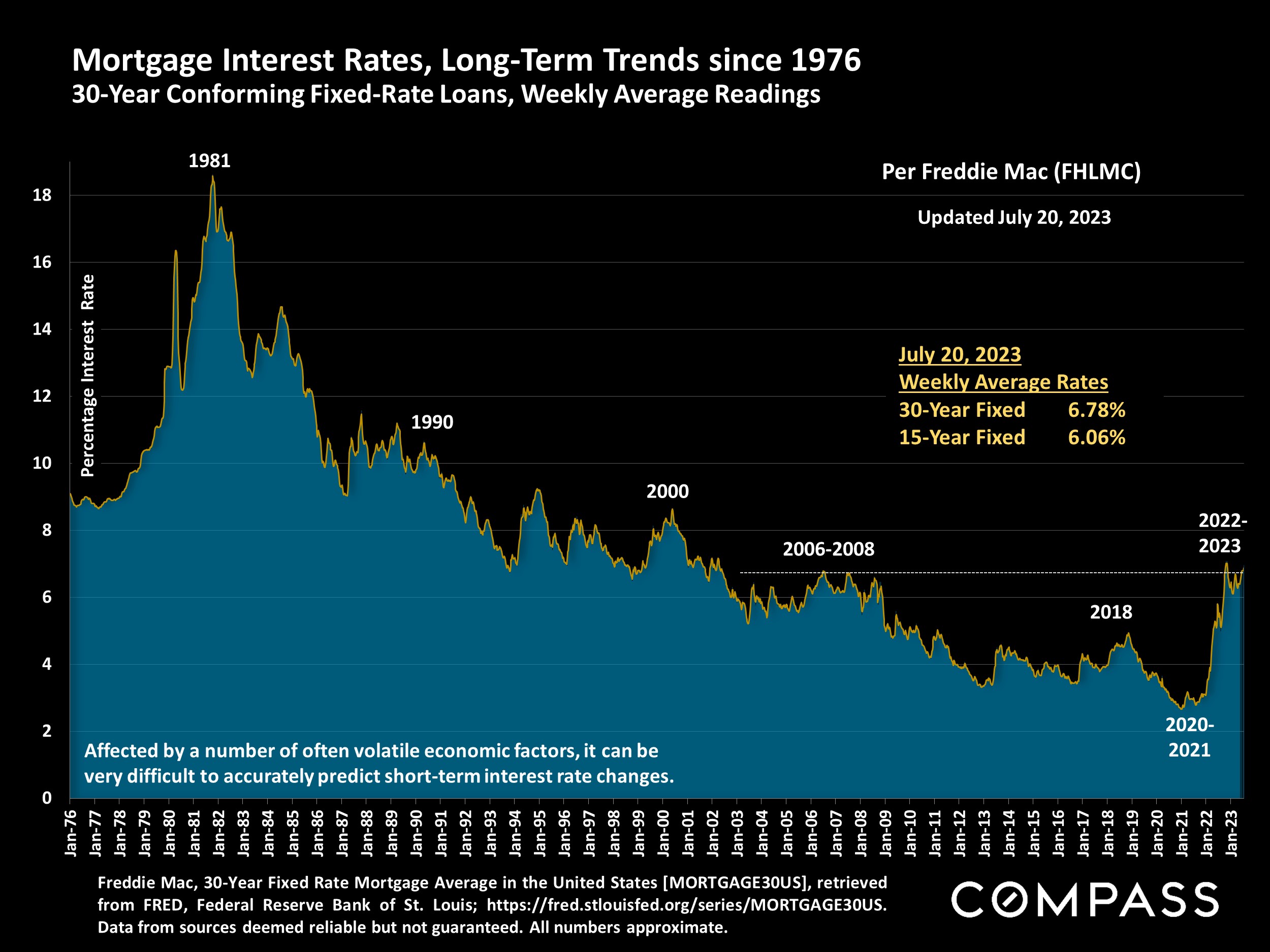

A long-term illustration of interest rates: Over the past year, after the dramatic rise in early 2022, 30-year fixed rates have generally ranged between 6% and 7%.

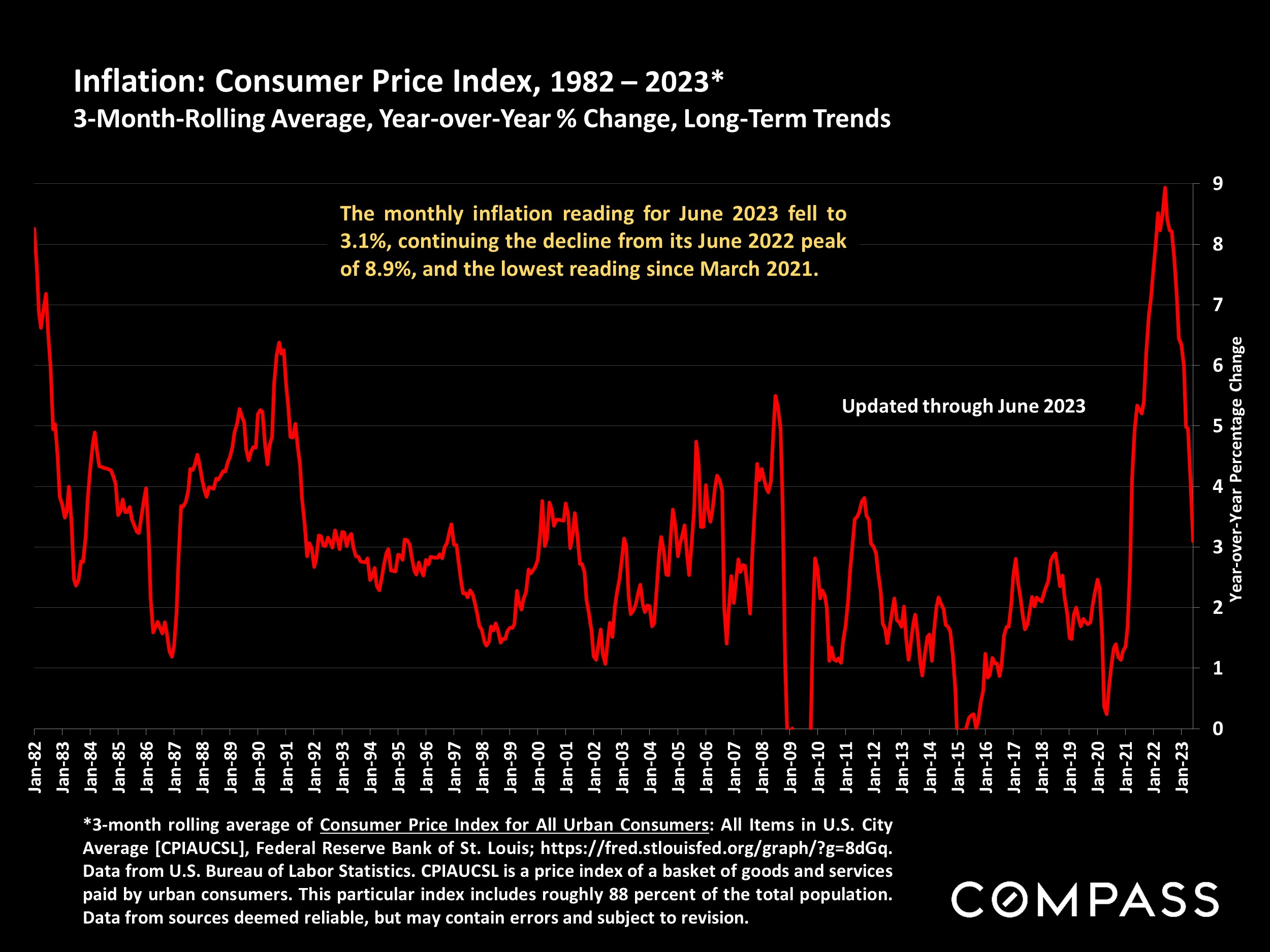

Inflation became a critical economic dynamic in the last 18 months, soaring to a 4-decade high in June 2022, then falling quickly since.

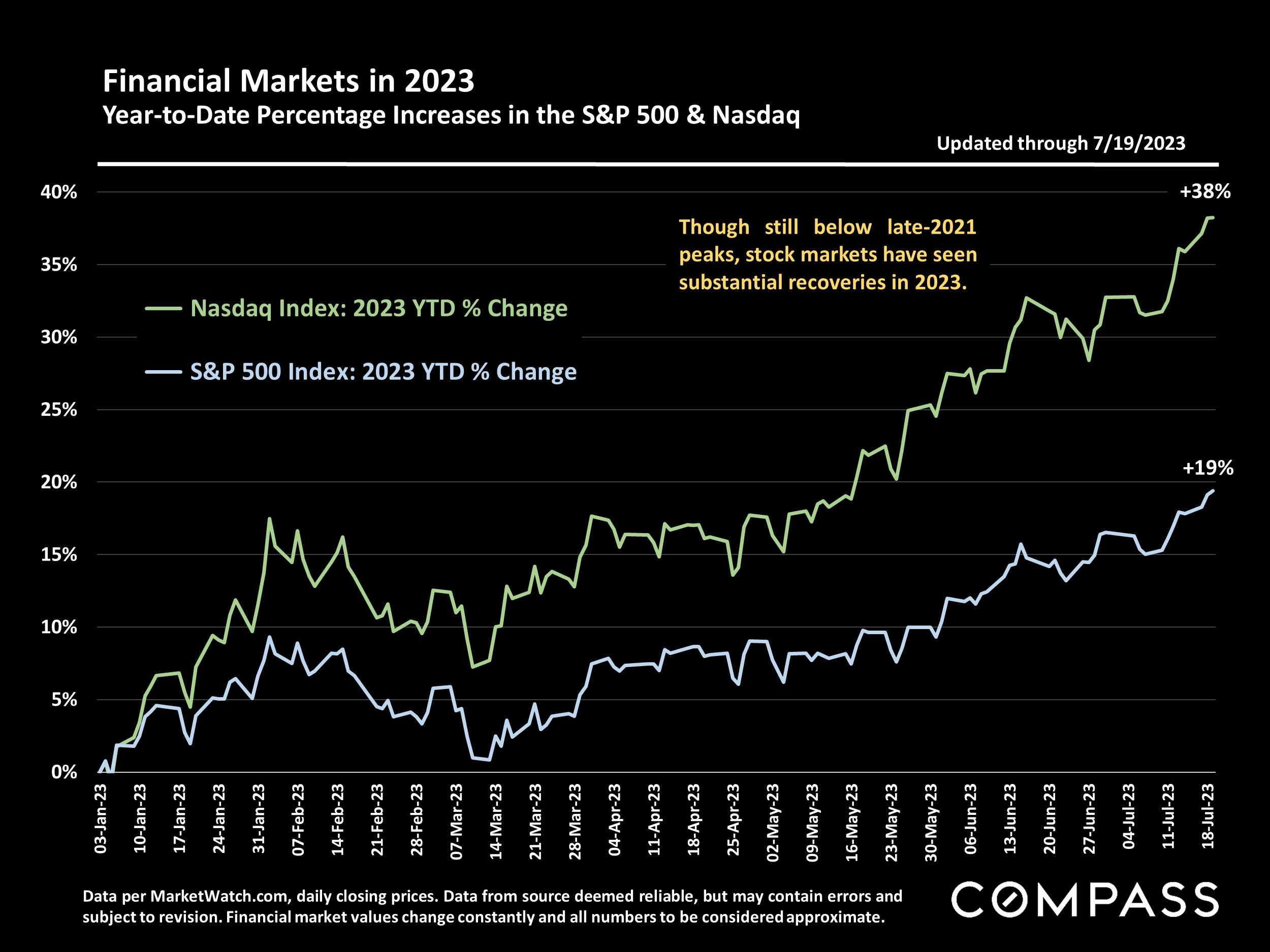

Financial markets have soared in 2023, deeply impacting household wealth - a huge factor in housing markets, especially in higher price segments.

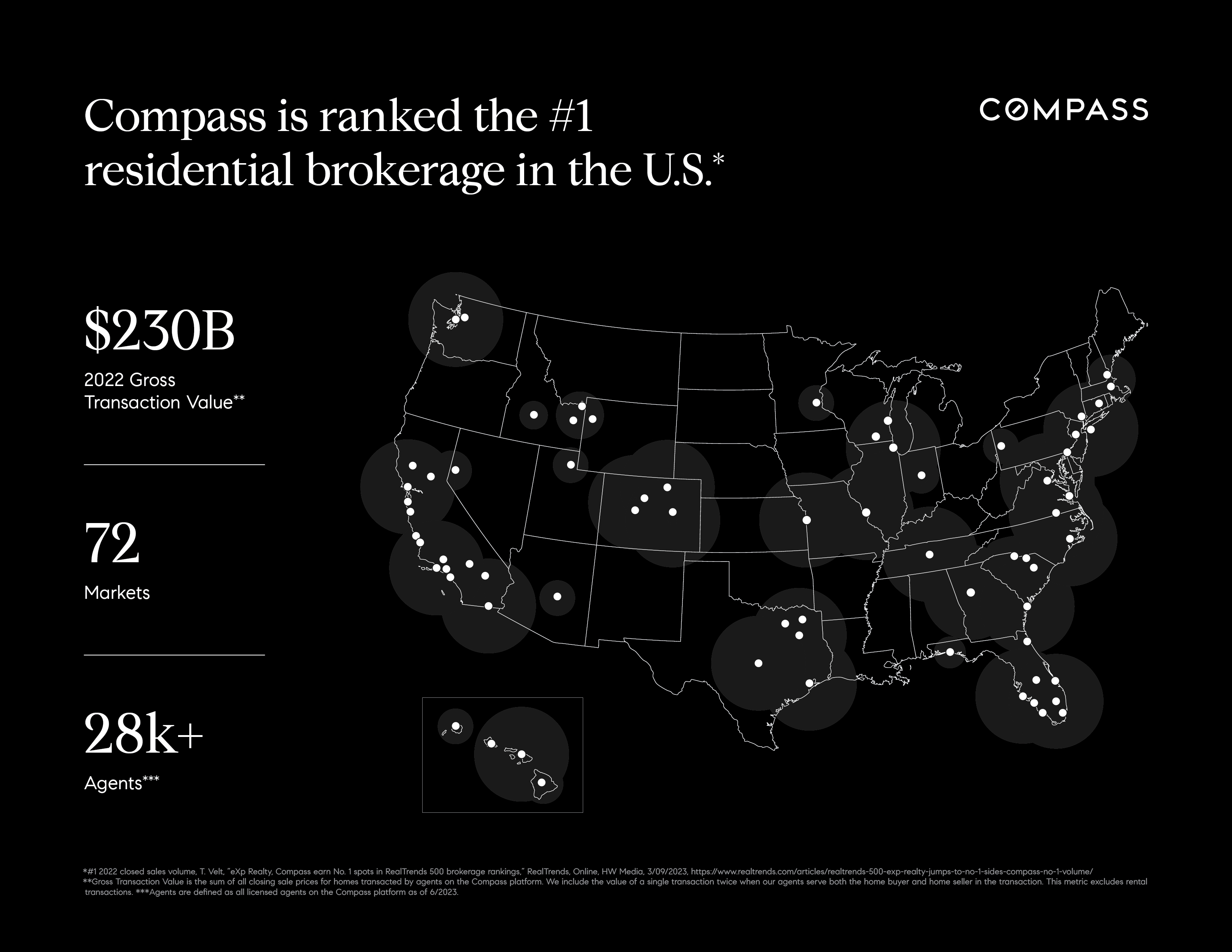

According to RealTrends, Compass ranks 1st by dollar-volume, U.S. home sales.

National and regional statistics are generalities, essentially summaries generated by thousands of unique, individual listings and sales occurring across different market segments. They are best seen not as precise measurements, but as broad, comparative indicators with reasonable margins of error. Anomalous fluctuations in statistics are not uncommon, and last period data should be considered preliminary estimates which may be revised in future updates. Different analytics programs sometimes define standard statistics - such as "active listings," "days on market," and "months supply of inventory" - differently: What is most meaningful are not specific numeric calculations but the trends they illustrate. Data from sources deemed reliable, but may contain errors, and subject to revision. All numbers to be considered approximate, and how these analyses apply to any particular property is unknown without a specific comparative market analysis.

Compass is a licensed real estate broker. All material is intended for informational purposes only and is compiled from sources deemed reliable but is subject to errors, omissions, changes in price, condition, sale, or withdrawal without notice. No statement is made as to the accuracy of any description or measurements (including square footage). This is not intended to solicit property already listed. No financial or legal advice provided. Equal Housing Opportunity. Photos may be virtually staged or digitally enhanced and may not reflect actual property conditions.

Garett's experience is why his clients are excited to refer his services to their family, friends and colleagues. Garett's strengths are prompt communication, service to his clients, as well as trust and commitment.